High-income taxpayers, including plastic and cosmetic surgeons, have historically seen a higher degree of examined returns.

Just about every plastic surgeon has friends, family members, or colleagues who are extremely aggressive when it comes to the tax deductions they claim on their income tax returns. In fact, every year around this time, they are all too willing to share the expenses they plan on taking as deductions and the reasons why they believe they are entitled to do so.

This article will help raise your audit awareness by alerting you to several red flags that might increase your chances of being subject to an IRS audit.

THE TAX GAP

One issue that the IRS has become very concerned with is the “tax gap,” which is the difference between the total taxes that should have been remitted and the amount of tax revenues actually collected.

The IRS most recently estimated the tax gap for 2001 and determined that tax revenues fell short by approximately $345 billion that year. Of that amount, 75% of the tax gap was due to small business owners and self-employed individuals.

The IRS has acknowledged that it cannot “audit its way out of the tax gap.” Even so, audits remain an important compliance tool. To make the most of its available resources, the IRS has taken steps to streamline the audit process while trying to better select which returns to audit. Although every taxpayer is thrilled when an audit ends as a “no change,” the IRS prefers that those tax returns never get selected in the first place.

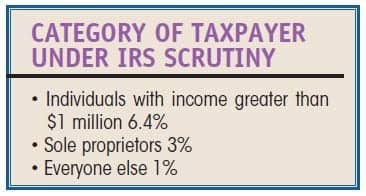

AUDIT STATISTICS

The IRS acknowledged back in 2008 that it will bring in almost $50 billion in tax revenues on a $10 billion budget. Even with results like that, there are no plans in place to significantly expand the IRS’ budget, so it needs to be very careful as to which returns are selected for audit.

Currently, the IRS is auditing the following groups of taxpayers each year:Individuals with an income greater than $1 million (6.4%), sole proprietors (3%), and everyone else (1%).

TRUST BUT VERIFY

One of the IRS’ long-term goals is to move away from traditional audits to more of a “trust but verify” environment. The service has observed that the tax gap is greatly reduced in areas where there is third-party verification, such as W2s to report wages, 1098s to report mortgage interest, or social security numbers for dependents.

A big challenge for the government, however, is to find a source of third-party verification that covers small businesses and self-employed individuals.

TYPES OF AUDITS

There are three basic types of audits: correspondence audits, office audits, and field audits.

In a correspondence audit, you mail your records to the IRS. In an office audit, you bring in your records to the IRS for examination. In a field audit, the examination takes place at your office or your representative’s office. Until the tax gap is brought under control, expect the IRS to rely on audits as a deterrent against noncompliance with the current tax laws. For that reason, let’s take this opportunity to augment your audit awareness.

AUGMENT YOUR AUDIT AWARENESS

The following are areas in which the IRS is currently focusing its auditing efforts:

1) Failure to report all taxable income.

If there appears to be a discrepancy with information reported from third parties (1099s and W2s), or if any information available may indicate your return is not completely accurate (public records, newspaper or magazine articles), then your chances of being audited greatly increase.

2) Claiming a home office deduction.

If a portion of your home is used regularly and exclusively in connection with your trade or business, you can take this deduction, which may include but is not limited to the following: rent, mortgage interest, real estate taxes, utilities, and phone bills.

However, according to the IRS, “To qualify under the exclusive use test, you must use a specific area of your home only for your trade or business [including for managerial and administrative tasks]. And to qualify under the regular use test, you must use a specific area of your home for business on a continuing basis.”

To claim the home office deduction, you need to complete and attach a Form 8829, Expenses for Business Use of Your Home, to your federal income tax return. On that tax form, you will prorate your allowable household costs by the percentage of your home that is used in connection with your business.

You make this calculation by dividing the square footage of your office by the total square footage of your home. Since this can be a large deduction and many of the people claiming this deduction don’t meet the criteria, it is always on the IRS radar screen.

3) Medical and dental expenses.

If you paid certain medical and dental expenses this year for yourself, your spouse, or your dependents, and were not reimbursed, then you may be eligible to claim the medical and dental expense deduction. Unfortunately, the hurdle for claiming this deduction is high. In order to claim a deduction for medical expenses, you must itemize deductions on Schedule A of your federal income tax return and your medical expenses must exceed 7.5% of your adjusted gross income (AGI).

If audited, the IRS requests copies of canceled checks, receipts, or statements for all medical savings accounts; medical and dental expenses (including medical insurance) showing the person for whom each expense was incurred; along with any insurance or employment reimbursement records. It also wants a copy of your medical insurance handbook or policy describing the benefits and reimbursement policy and verification of premium costs.

For prescription drug expenses, you’ll need to send copies of statements or receipts showing the prescription numbers, names of drugs, costs, and date purchased.

For other expenses—including capital improvements, equipment, transportation, and lodging—it will ask you to send proof of payment and statements to show costs and medical requirement.

4) Charitable donations.

A charitable gift is a contribution of cash or property to, or for the use of, a qualified charity. A gift is “for the use of” an organization when it is held in a legally enforceable trust for the qualified organization or in a similar legal arrangement.

To receive a tax deduction for your gift, you must itemize your deductions and make the gift to a qualified organization, not to a specific person. If you claim large charitable deductions that are disproportionately large compared to your income, you may find yourself under the scrutiny of the IRS.

If audited, the IRS will request copies of canceled checks and receipts for contributions to charitable organizations. If the contribution was other than money, it will ask you to provide the name and address of the charitable organization, as well as a description of the items contributed. If the donation was valued at more than $5,000, and an appraisal may be required by Form 8283 (Non-Cash Charitable Contributions), you’ll need to send a copy of the appraisal showing the fair market value of each item on its contribution date, as well as evidence of its original cost.

Finally, if you claimed expenses for attending a convention or similar activity, you’ll need to provide a statement showing you were an official representative of the organization; as well as the organization’s reimbursement policy, expense receipts, and an itinerary or agenda for the activity.

5) Employee business expenses.

To be deductible, employee business expenses must be (1) paid or incurred during your tax year, (2) for carrying on your trade or business of being an employee, and (3) ordinary and necessary. An ordinary expense is one that is common and accepted in your field of business, trade, or profession. A necessary expense is one that is helpful and appropriate (but not necessarily indispensable) for your business.

For starters, the IRS will request that you provide a copy of your employer’s reimbursement policy or a letter from the employer explaining what expenses are reimbursed. The letter should also indicate whether it is an “accountable” or “nonaccountable” reimbursement plan.

If your employer does not have a reimbursement policy, you’ll be asked to provide a letter from your employer indicating what expense(s), if any, are reimbursed or that no reimbursement is authorized, as well as a statement as to whether or not reimbursement is included as income to you on your W2.

You will also need to forward a copy of any receipts for any expenses claimed greater than $75, receipts for any lodging expenses claimed, and copies of logs, diaries, or other records showing all expenses incurred, job locations, and dates you were at each location. For meals and entertainment, these records should detail the business purpose and the business relationship.

The IRS will also ask you to verify the total mileage for any car for which deductible mileage was claimed. This can be from two repair receipts, inspection slips, or any other records showing total mileage for the year.

6) Mortgage interest deduction.

If you itemize deductions, you can generally deduct “qualified residence interest” you pay on certain home mortgages taken in connection with your primary residence and a second residence. This deduction generally applies only to interest on mortgages to buy, build, or improve your primary or secondary residence, or to up to $100,000 of home equity loans used for any purpose.

The current rules allow you to write off the interest paid on the first $1,000,000 of mortgage indebtedness. The other type of mortgage interest tax deduction stems from the home equity debt—that is defined as any debt that is other than the home acquisition debt and cannot exceed $100,000.

Assuming a rate of 6%, that means you can claim $66,000 of mortgage interest on your income tax return. If the amount of interest claimed exceeds $60,000, the IRS may want you to provide documentation supporting your deduction.

Expect that you will be required to submit each Form 1098, Mortgage Interest Statement, as well as your monthly mortgage bills, and (perhaps) your HUD1 Settlement Statement reflecting the original amount borrowed when you purchased or refinanced your home.

CONCLUSION

While there is no way to know exactly what will trigger an audit in a given year, past years have seen an apparent focus on self-employed, those claiming home office deductions, and those with itemized deductions exceeding the average for individuals with similar income levels—and, more recently, a large mortgage interest deduction.

In addition, high-income taxpayers, including plastic and cosmetic surgeons, have historically seen a higher degree of examined returns. That said, the trick to minimizing your federal tax burden is to understand the rules as best you can, and then make the most of your tax planning opportunities.

Andrew D. Schwartz, CPA, is a partner in the Boston CPA firm Schwartz & Schwartz, PC, and is also the founder of the MDTAXES Network, a national network of CPAs specializing in tax and accounting services for the health care profession. He can be reached at .

Lawrence B. Keller, CLU, ChFC, CFP, is the founder of Physician Financial Services, a New York-based firm specializing in income-protection and wealth-accumulation strategies for physicians. He can be reached at